Article Summary: California’s high rate of uninsured motorists makes carrying robust State Farm uninsured and underinsured motorist (UM/UIM) coverage essential for financial protection. State law requires insurers to offer these policies, which compensate for medical bills, lost wages, and pain and suffering when an at-fault driver lacks sufficient liability insurance. While UM coverage addresses drivers with no insurance, UIM coverage bridges the gap when an at-fault party’s policy limits are exhausted before covering all damages. Policyholders should aim to match their UM/UIM limits with their liability limits to ensure adequate recovery after catastrophic accidents, as California’s minimum requirements of $15,000 per person often fall short of modern medical costs. Filing a claim involves prompt notification to State Farm and thorough documentation of injuries, though adjusters may offer settlements that do not fully reflect total losses. Because insurance companies prioritize their own interests, understanding the nuances of the California Insurance Code and the arbitration process is vital. Seeking legal expertise can help navigate coverage gaps and push back against lowball offers or claim denials, ensuring injured motorists receive the maximum compensation allowed under their specific policy terms.

California State Farm Uninsured Motorist Claims

Getting hit by a driver who has no insurance, or not enough of it, is one of the most frustrating situations a California motorist can face. You did nothing wrong, yet you’re stuck with medical bills, a damaged vehicle, and no clear path to compensation. Understanding your State Farm uninsured motorist coverage California policy before that moment arrives can be the difference between financial recovery and thousands of dollars coming out of your own pocket.

California law requires insurers to offer uninsured motorist (UM) and underinsured motorist (UIM) coverage with every auto policy, but what State Farm actually provides, and what you’re entitled to under your specific plan, isn’t always straightforward. Coverage limits, stacking rules, and the claims process all carry details that trip up policyholders regularly. Worse, insurance adjusters don’t always explain your options in a way that serves your best interest, which can leave you underinsured without realizing it.

At Steven M. Sweat, Personal Injury Lawyers, APC, we’ve spent over 25 years representing injured Californians in disputes with insurance companies, including fights over UM and UIM claims. From our Los Angeles office, we’ve seen firsthand how coverage gaps and lowball settlement offers affect real people dealing with serious injuries. That experience drives this guide, we want you to understand exactly what your State Farm policy covers, how California law shapes your rights, and what steps to take if you’re ever hit by an uninsured or underinsured driver.

This article breaks down State Farm’s uninsured motorist coverage in California from top to bottom: state minimum requirements, how UM and UIM coverage actually work, what your policy options look like, and how to protect yourself if you need to file a claim or push back against a denial.

Why UM and UIM matter in California

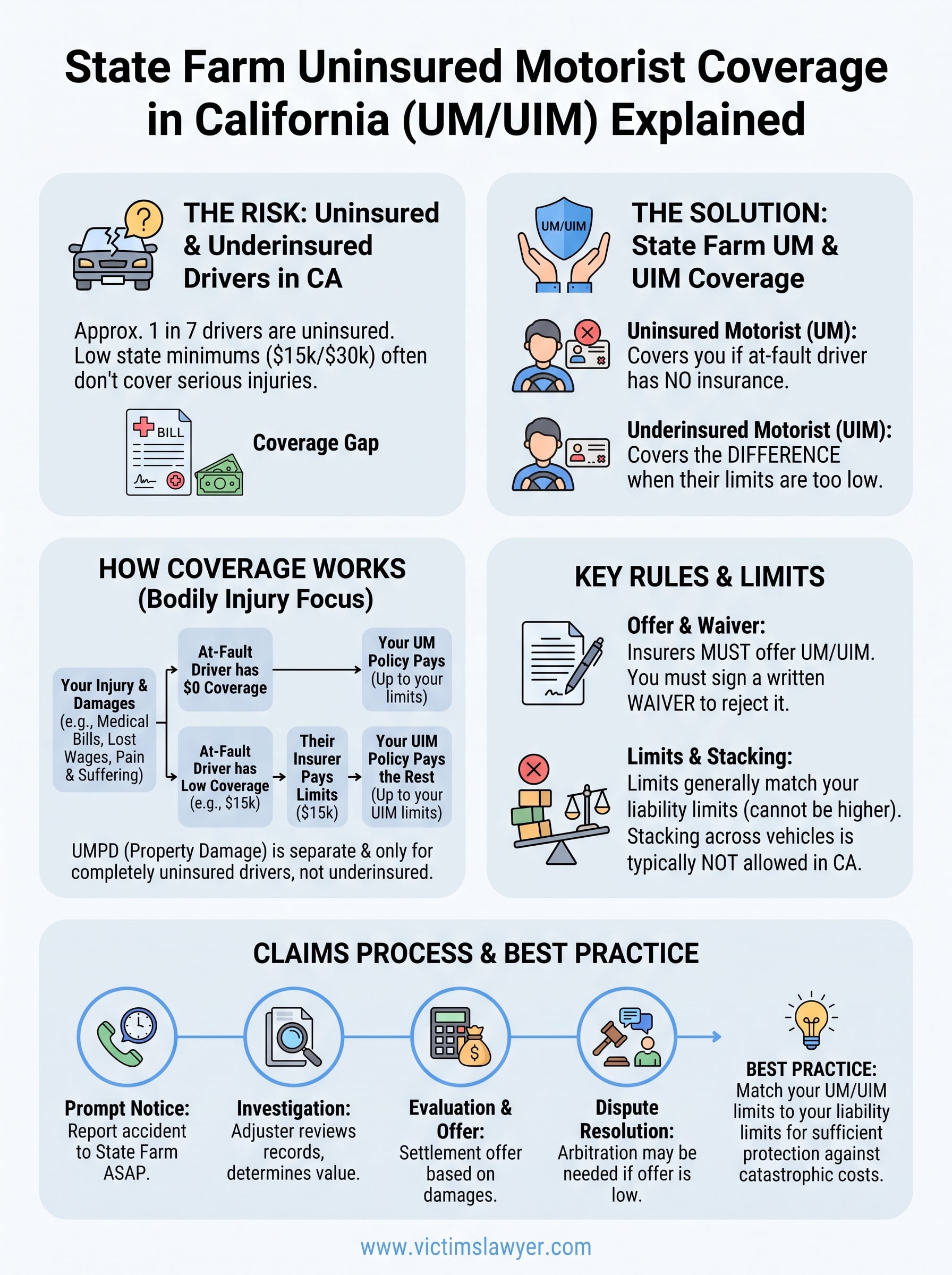

California has one of the highest rates of uninsured drivers in the country. According to the Insurance Research Council, roughly 1 in 7 drivers on California roads carries no auto insurance at all. That means every time you get behind the wheel, there is a real statistical chance that the other person involved in a collision won’t have coverage to pay for your injuries or vehicle damage.

The uninsured driver problem on California roads

The state’s minimum liability requirements are also part of the problem. California currently sets its minimums at $15,000 per person and $30,000 per accident for bodily injury, amounts that haven’t kept pace with the actual cost of modern medical care. Even when a driver carries insurance, those limits can disappear quickly if you suffer a broken bone, a head injury, or any condition requiring surgery or extended rehabilitation.

If the driver who hits you has no insurance or only the bare legal minimum, your ability to recover fair compensation depends heavily on the UM and UIM coverage attached to your own policy.

Your state farm uninsured motorist coverage california policy exists specifically to fill that gap. Without it, your only legal option after a crash with an uninsured driver is often to sue the at-fault driver directly, which works only if that person has personal assets worth pursuing, and most people who drive without insurance don’t.

What underinsured means for your recovery

Underinsured motorist coverage addresses a different but equally serious problem. A driver can be fully insured under California law yet still carry limits far too low to cover a serious accident. If their policy pays out $15,000 and your medical bills total $80,000, you face a $65,000 shortfall with no straightforward way to recover it.

Your UIM coverage steps in once the at-fault driver’s liability policy is exhausted. It pays the difference between what their insurer paid and your actual damages, up to your own UIM policy limits. This protection matters most in accidents involving catastrophic injuries like traumatic brain injuries, spinal damage, or long-term disability, situations where treatment costs run well into six figures and lost income compounds the financial pressure over months or years.

What California law requires and allows

California Insurance Code Section 11580.2 requires every auto insurer, including State Farm, to offer uninsured motorist coverage with any policy sold in the state. The law doesn’t force you to buy it, but your insurer must offer it and must get your written rejection if you decide to decline. If no signed waiver exists in your file, your insurer may owe you UM coverage even if you didn’t pay for it explicitly.

How the offer and rejection process works

When you buy or renew a State Farm policy, the company must offer UM and UIM coverage at limits that match your liability coverage by default. You can choose lower limits, but you cannot set UM or UIM limits higher than your liability limits. If you want to reject coverage entirely, you must sign a written waiver confirming that choice. That waiver carries legal weight, so read it carefully before you sign.

Insurers are required by California law to make this offer in writing, which means you have a documented record of what you were offered and what you accepted or declined.

Limits and stacking rules

Your state farm uninsured motorist coverage california policy sets a ceiling on what you can recover per person and per accident. California generally does not allow stacking of UM limits across multiple vehicles listed on the same policy. Key factors that shape your coverage ceiling include:

- The per-person and per-accident limits printed on your declarations page

- Whether your policy contains specific anti-stacking language

- How your UIM limits compare to the at-fault driver’s actual liability payout

What State Farm UM and UIM can cover

Your state farm uninsured motorist coverage california policy can pay for a range of losses that the at-fault driver’s insurance would have covered if they had carried enough of it. The specific categories of compensation available depend on your policy’s language and the limits you selected, but the coverage is designed to put you in roughly the same position you would have been in if the other driver had been properly insured.

Bodily injury losses

State Farm’s UM and UIM coverage applies primarily to physical injuries you sustain in the crash. This includes medical bills for emergency care, surgeries, hospital stays, physical therapy, prescription medications, and any future treatment your doctor identifies as necessary. Beyond direct medical costs, you can also claim lost wages if your injuries kept you out of work, and compensation for pain and suffering based on the severity and duration of your physical and emotional harm.

Serious injuries like traumatic brain injuries or spinal damage often produce long-term costs that far exceed initial estimates, which is exactly why higher UM limits matter.

Property damage coverage

California allows you to purchase uninsured motorist property damage (UMPD) coverage separately from UM bodily injury coverage. UMPD through State Farm can pay to repair or replace your vehicle when an uninsured driver causes the collision. However, UMPD does not cover underinsured drivers, only those with no coverage at all. If the at-fault driver has some insurance but not enough, your collision coverage handles the vehicle damage instead.

How a State Farm UM or UIM claim works

Filing a state farm uninsured motorist coverage california claim follows a specific process, and how quickly you move through each step affects the strength of your case. You must notify State Farm promptly after the accident, provide documentation of your injuries and losses, and cooperate with their investigation. Delays or incomplete records give adjusters justification to reduce or deny your claim.

Notifying State Farm after the crash

You should contact State Farm as soon as possible after an accident involving an uninsured or underinsured driver. The company requires prompt notice as a condition of coverage, and most policies set a specific timeframe for reporting. When you call, have the other driver’s information ready, including their name, license plate, and any insurance details they provided, even if that policy turned out to be insufficient.

Failing to report within your policy’s required window can give State Farm grounds to deny coverage, even when your underlying claim is valid.

What happens during the investigation

State Farm will assign an adjuster to review your medical records, repair estimates, and police report. The adjuster’s job is to evaluate your damages and determine what the company owes under your policy limits. You have the right to submit your own documentation, including independent medical evaluations and expert opinions, to support a higher valuation if the initial offer falls short.

Disputes over settlement amounts in UM and UIM claims are common. If you and State Farm cannot reach agreement, your policy may include an arbitration clause that determines the final outcome outside of court.

How much UM and UIM you may need

The state minimums for UM coverage in California start at $15,000 per person and $30,000 per accident, which mirrors the liability minimums. Those numbers sound reasonable until you price out an emergency room visit, a week in the hospital, and two months of physical therapy. Choosing your limits based only on what the law requires leaves a significant gap between what you can claim and what a serious injury actually costs.

Your UM and UIM limits should reflect the real cost of a catastrophic injury, not the legal floor set by the state.

Matching your limits to your actual exposure

Your state farm uninsured motorist coverage california policy lets you set UM and UIM limits up to the amount of your liability coverage. A practical approach is to match your UM and UIM limits to your liability limits, so you carry the same level of protection whether you’re the one causing harm or the one absorbing it. If you carry $100,000/$300,000 in liability coverage, your UM and UIM limits should mirror that.

Your specific circumstances also shape how much coverage makes sense. Consider these factors when reviewing your limits:

- Your health insurance: Gaps in medical coverage increase your dependence on UM payouts

- Your income and time off work: Higher earners lose more when injuries sideline them

- Your commute and driving habits: More time on the road means more exposure to uninsured drivers

- Your savings cushion: Less personal savings means you absorb more risk with lower limits

Next Steps After an Uninsured Driver Crash

After a crash with an uninsured or underinsured driver, your first priority is documenting everything at the scene: photos, witness contact details, the police report number, and any insurance information the other driver provides. Report the accident to State Farm promptly and preserve all medical records and bills from the start.

Your state farm uninsured motorist coverage california policy gives you a path to compensation, but insurance adjusters work for State Farm, not for you. If the settlement offer feels low, or if your claim is delayed or denied, you have the right to push back with legal support.

At Steven M. Sweat, Personal Injury Lawyers, APC, we handle UM and UIM disputes for injured Californians on a contingency basis, meaning no fees unless we recover money for you. Contact our team today for a free consultation and find out exactly what your claim may be worth.