You’re recovering from a car accident, your medical bills are climbing, and the at-fault driver’s insurance maxes out at $15,000. That doesn’t come close to covering your losses. This is exactly when the question hits: what does underinsured motorist coverage pay for, and does your own policy actually protect you? The answer matters more than most drivers realize, and it can mean the difference between full financial recovery and thousands of dollars out of pocket.

At Steven M. Sweat, Personal Injury Lawyers, APC, we’ve spent over 25 years representing accident victims across Los Angeles and throughout California who find themselves in this exact situation. We’ve seen firsthand how underinsured motorist (UIM) coverage works in practice, what it actually pays for, where the gaps are, and how insurance companies try to minimize what they owe. It’s one of the most misunderstood parts of an auto policy, and getting it wrong can be costly.

This article breaks down UIM coverage in plain terms: what expenses it covers, what it doesn’t, how California law applies, and what to do when the at-fault driver’s policy falls short of your actual damages.

Why underinsured motorist coverage matters in California

California has some of the busiest roads and highest accident rates in the country. Despite that, the state only requires drivers to carry a minimum of $15,000 in bodily injury liability coverage per person and $30,000 per accident. Those limits were set decades ago and have not kept pace with the actual cost of medical treatment, lost income, or long-term care.

A single emergency room visit after a serious crash can easily exceed California’s minimum liability requirement before you even account for surgery, physical therapy, or lost wages.

California’s minimum coverage problem

When the at-fault driver carries only minimum liability limits, their policy runs out fast. A broken leg, a concussion, or any injury requiring surgery can generate bills well above $15,000. If that driver’s insurance pays out its policy limit and you still have $80,000 in medical expenses, the remaining balance falls on you unless you have UIM coverage in place.

Your own UIM coverage steps in to bridge that gap. It pays the difference between what the at-fault driver’s policy covers and your actual documented losses, up to your own UIM policy limit. This benefit does not come from the other driver’s insurer; it comes from the coverage you purchased through your own policy.

Why more drivers are underinsured than you think

Many drivers in California choose minimum coverage simply to keep their monthly premiums low. That decision directly affects you if one of them causes your accident. According to the Insurance Research Council, roughly 1 in 8 drivers nationwide carries inadequate or no liability coverage, and in dense urban areas like Los Angeles, that number trends higher.

Understanding what does underinsured motorist coverage pay for in this environment is a practical question that shapes how much compensation you can realistically recover after a serious crash in California.

What underinsured motorist coverage pays for

UIM coverage steps in when the at-fault driver’s liability policy is exhausted. Understanding what underinsured motorist coverage pays for helps you know exactly what to document and claim after a serious crash. Your own UIM policy covers a wide range of actual, verifiable losses that the at-fault driver’s insurance left unpaid.

The more thoroughly you document your losses, the stronger your UIM claim becomes.

Covered damages and expenses

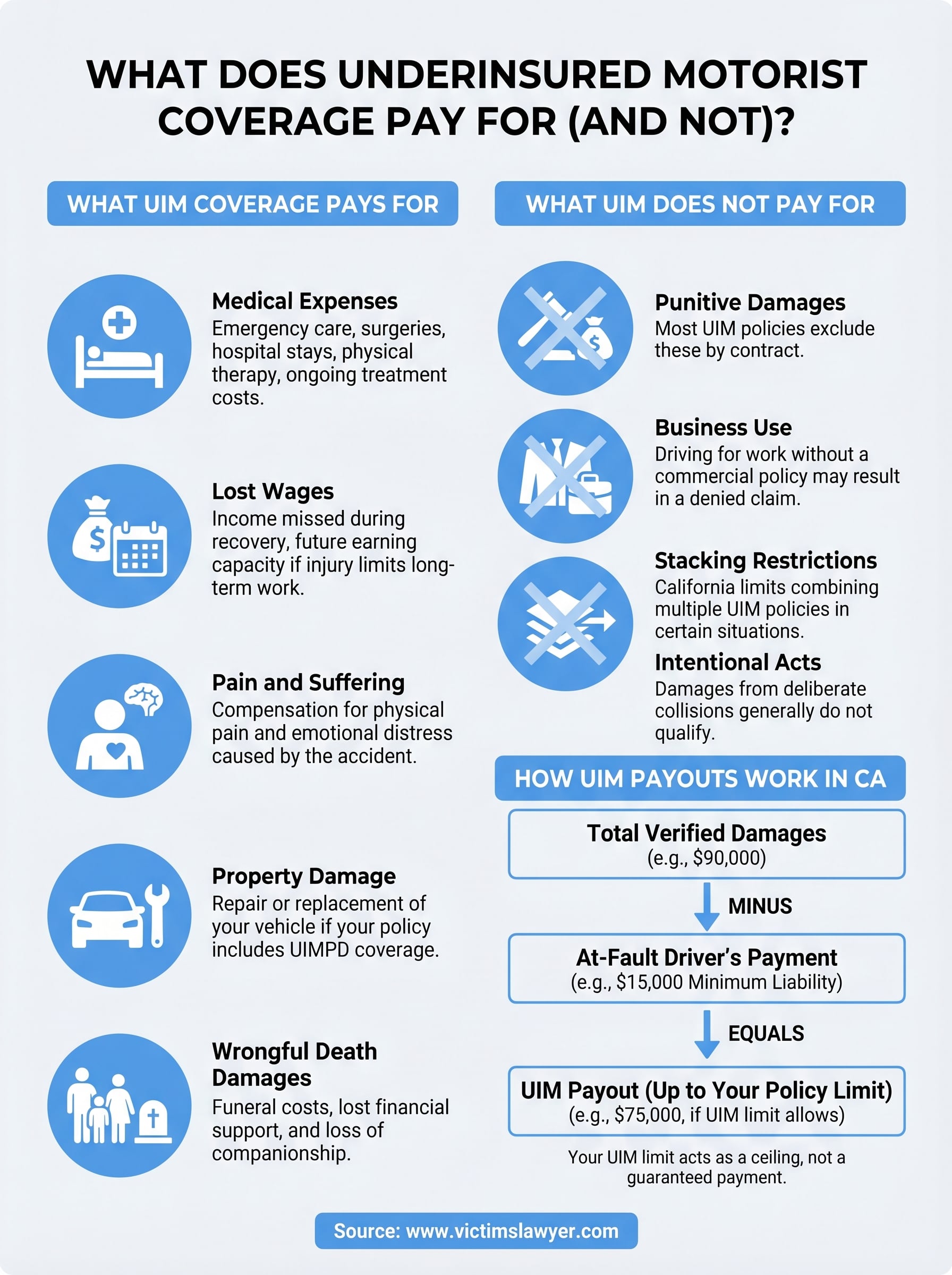

Your UIM policy can pay for the following categories of loss:

- Medical expenses: Emergency care, surgeries, hospital stays, physical therapy, and ongoing treatment costs

- Lost wages: Income you missed while recovering, including future earning capacity if your injury limits long-term work

- Pain and suffering: Compensation for physical pain and emotional distress caused by the accident

- Property damage: Repair or replacement of your vehicle if your policy includes UIMPD coverage

- Wrongful death damages: Funeral costs, lost financial support, and loss of companionship for surviving family members

Each category requires supporting documentation such as medical records, pay stubs, and repair estimates. Your UIM claim draws directly from your own policy limits, not the at-fault driver’s insurer, so knowing your coverage amount before you negotiate is critical.

What underinsured motorist coverage does not pay for

UIM coverage has real limits, and knowing what it excludes is just as important as knowing what does underinsured motorist coverage pay for. Your UIM policy will not pay if the at-fault driver actually carries adequate liability limits to cover your full losses, because UIM only activates when their coverage falls short of your verified damages.

UIM coverage is not a catch-all policy. It only activates when the at-fault driver’s limits are genuinely insufficient to compensate your documented losses.

Common exclusions to know

Several specific situations fall outside UIM coverage, and they catch many accident victims off guard:

- Punitive damages: Most UIM policies exclude these by contract

- Business use: Driving for work without a commercial policy may result in a denied claim

- Stacking restrictions: California limits your ability to combine multiple UIM policies in certain situations

- Intentional acts: Damages from deliberate collisions generally do not qualify

Your insurer may also dispute the value of your claim or argue that your injuries existed before the accident. These denials are common and often require a legal challenge to reverse. Understanding the exclusions before you file helps you build a stronger, better-documented claim from the start.

How UIM payouts work in California

California UIM payouts follow a specific calculation that determines how much your policy actually owes you. Your insurer subtracts what the at-fault driver’s policy already paid from your total verified damages, then pays the remaining balance up to your own UIM policy limit. This means your UIM limit acts as a ceiling, not a guaranteed payment amount.

The gap between what the at-fault driver’s insurance pays and your total losses is the figure that drives your UIM payout.

The offset rule and policy limits

California insurers apply an offset rule when calculating UIM payouts. If the at-fault driver carries $15,000 in liability coverage and your verified losses total $90,000, your UIM policy covers up to $75,000 of the remaining balance, assuming your UIM limit is high enough to reach that amount. If your UIM limit is only $50,000, that becomes the hard cap on what you can collect.

Understanding what does underinsured motorist coverage pay for in practical terms means knowing your own policy limits before you settle any claim. Accepting the at-fault driver’s payout without first consulting an attorney can waive your right to pursue additional UIM compensation.

How to file a UIM claim step by step

Filing a UIM claim requires specific steps taken in the correct order. Skipping a step or waiting too long can give your insurer grounds to deny or reduce your payout. California’s statute of limitations for UIM claims is generally two years from the accident date, which means you need to act without delay.

Missing a deadline or misordering your steps can permanently reduce what does underinsured motorist coverage pay for in your specific situation.

Steps to follow after the at-fault driver’s policy is exhausted

Once the at-fault driver’s insurer pays out its full liability limit, you can formally open your UIM claim. Working with an attorney at this stage gives you the best chance of recovering the full value of your documented losses. Follow these steps:

- Notify your insurer: Report the accident to your own carrier immediately, even before the at-fault driver’s insurer pays out.

- Gather documentation: Collect medical records, bills, pay stubs, and repair estimates.

- Get written confirmation: Obtain proof of the at-fault driver’s policy limits and their insurer’s payment.

- Submit your UIM claim: File formally with all supporting documents attached.

- Negotiate or litigate: If your insurer disputes the value, push back with legal support.

Next steps after an underinsured crash

When the at-fault driver’s policy runs dry, you need to move quickly and deliberately. Notify your own insurer right away, preserve every piece of documentation you have, and confirm the at-fault driver’s policy limits in writing before accepting any settlement. Understanding what does underinsured motorist coverage pay for is only useful if you act on that knowledge before deadlines close.

An experienced attorney makes a measurable difference at every stage of this process. Your insurer has teams trained to reduce what they pay out, and without legal support, you risk accepting far less than your claim is actually worth. Medical records, lost wage documentation, and expert testimony all strengthen your position during negotiation or arbitration.

If you were hurt in a crash and the other driver’s coverage fell short, talk to a California personal injury attorney at Steven M. Sweat, Personal Injury Lawyers, APC before you sign anything.