Filing AAA insurance claims after an accident should be straightforward, but the reality is often more complicated than policyholders expect. Between gathering documentation, meeting deadlines, and communicating with adjusters, even a simple fender-bender claim can turn into a drawn-out process that leaves you frustrated and undercompensated.

At Steven M. Sweat, Personal Injury Lawyers, APC, we’ve spent over 25 years helping injured Californians deal with insurance companies, including AAA. We’ve seen firsthand how claims get delayed, undervalued, or outright denied, and we know exactly where the process tends to break down for people who are already dealing with medical bills and lost wages.

Whether you’re filing a new claim, trying to track one that’s already in progress, or wondering why your settlement offer seems too low, this guide walks you through the entire AAA insurance claims process step by step. You’ll find specific instructions for auto, home, and life insurance claims, along with the contact numbers and online tools you need to get things moving. We also share practical tips drawn from our experience representing accident victims, so you can protect your rights from the start and recognize when it might be time to get a lawyer involved.

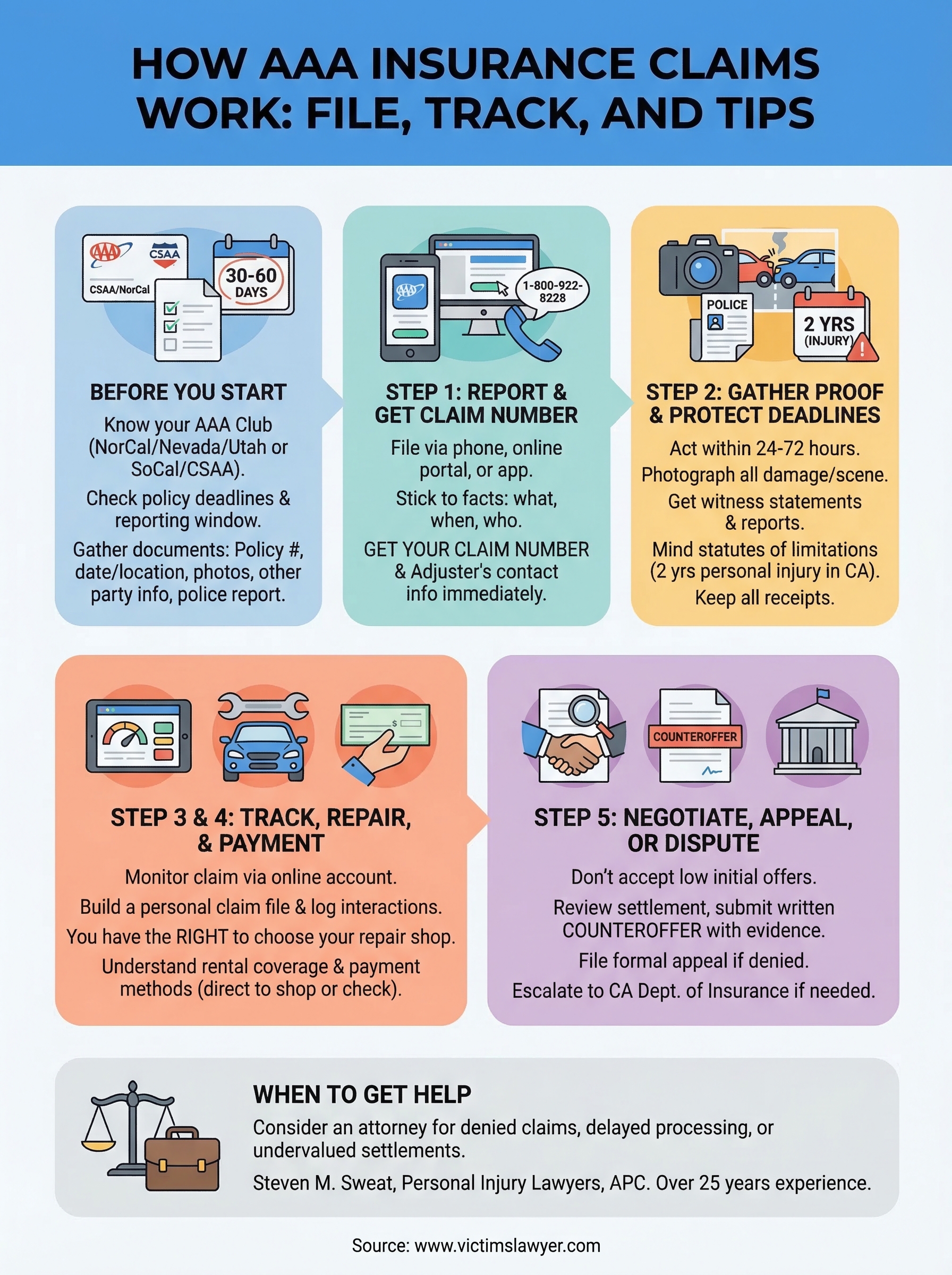

What to know before you start an AAA claim

AAA operates differently from most national insurers, and that difference matters when you’re about to file a claim. AAA is a federation of regional clubs, not a single unified insurance company. Depending on where you live in California, your policy may be issued by AAA Northern California, Nevada & Utah or AAA Southern California (CSAA Insurance Group). Both operate under the AAA brand, but they have separate claims departments, phone numbers, and online portals. Before you do anything else, check your insurance card or declarations page to confirm which club issued your policy.

AAA’s club structure and which company covers you

Your specific AAA club determines which claims process you follow. CSAA Insurance Group handles policies for members in Southern California, while AAA Northern California, Nevada & Utah covers the northern region. If you’re unsure which club you belong to, look at the top of your insurance ID card or declarations page. The issuing company name appears there, and getting this right saves you time and avoids misdirected calls.

Calling the wrong regional office is one of the most common delays policyholders run into, so confirm your issuing club before you dial.

Here is a quick reference for AAA’s two main California insurance entities:

| Region | Issuing Entity | General Claims Line |

|---|---|---|

| Southern California | CSAA Insurance Group | 1-800-922-8228 |

| Northern California | AAA Northern CA, NV & UT | 1-800-922-8228 |

Both regions share the same general claims line, but your call gets routed internally based on your policy number. Have your date of loss ready before you call to speed up that routing process.

Key deadlines and policy terms to check first

Every insurance policy includes a prompt reporting requirement, which means you are expected to notify AAA of a loss within a reasonable time after it occurs. For auto claims in California, most policies expect you to report within 30 to 60 days of the incident, though the exact language varies by policy. For home insurance claims, reporting timelines can be even tighter if the damage involves an ongoing condition like water intrusion. Pull out your declarations page and read the “duties after loss” section before you file.

Your policy also spells out your coverage limits, deductibles, and any exclusions that apply to your specific situation. For example, a standard auto policy may include collision, comprehensive, and liability coverage, but it will not cover a rental car unless you added that endorsement. Knowing exactly what you purchased before you file prevents unwanted surprises when the adjuster reviews your claim and helps you push back if coverage is denied on a technicality.

What to have ready before you file

Starting an AAA insurance claims process without your documents in order can slow everything down and put you in a weaker position from day one. Having your information organized before that first call or portal login shortens the intake process and gives the adjuster everything needed to open your file immediately. Gather the following before you reach out:

- Policy number and declarations page

- Date, time, and exact location of the incident

- Photos or video of all visible damage

- Names and contact information for any other parties involved

- A copy of the police or incident report, if one was filed

- Medical records or bills if injuries are part of the claim

- Witness names and contact information

With these items in hand, you walk into the process prepared rather than reactive.

Step 1. Report the claim and get a claim number

Once you have your documents ready, your first priority is to report the incident to AAA as quickly as possible. You can open AAA insurance claims through three channels: by phone, through the online portal, or through the AAA mobile app. All three methods produce the same outcome, a file in AAA’s system with a unique claim number assigned to your case. That claim number becomes your reference point for every conversation, email, and document submission going forward, so write it down the moment you receive it.

How to file by phone or online

Calling AAA’s claims line at 1-800-922-8228 is the fastest way to reach a live representative, and it works around the clock. When you call, the representative will ask for your policy number, the date and location of the loss, a brief description of what happened, and the contact information of anyone else involved. If you prefer to file online, log into your regional AAA account and navigate to the claims section. The online form walks you through the same questions in a structured format, and you can upload photos and documents directly at the time of filing, which saves you a follow-up step later.

Filing online or through the app also creates a written record of exactly what you reported on day one, which can protect you if the adjuster later questions the details.

Have the following ready before you report, regardless of the channel you choose:

- Policy number and named insured’s full name

- Date, time, and exact location of the incident

- A brief, factual description of what happened

- Names, contact details, and insurance information for other parties

- Police report number, if law enforcement responded

What to say when you first report

Keep your initial statement factual and limited to what you know for certain. Do not speculate about fault, minimize your injuries, or say something like “I’m fine” before you have seen a doctor. Adjusters are trained to use early statements during settlement negotiations, and an offhand comment can reduce your claim’s value before the process even gets started. Stick to the basic facts: what happened, when it happened, and who was involved.

After you receive your claim number, ask the representative for the name and direct contact information of your assigned adjuster. That person handles your file from this point forward, and having their direct line cuts out the hold time on every future call.

Step 2. Gather proof and protect your deadlines

The evidence you collect in the first 24 to 72 hours after an incident is often the most powerful evidence you’ll ever have. Damage is visible, memories are fresh, and witnesses are still reachable. Waiting even a few days can mean missing crucial details, and a weak evidentiary record directly reduces what AAA will pay on your claim.

What evidence to collect right now

Start documenting your loss before you move anything or have repairs made. Use your phone to photograph all visible damage from multiple angles, including wide shots showing the full scene and close-up shots showing specific points of impact. If your claim involves a vehicle, photograph all four sides, the interior if affected, and the surrounding area. For home insurance claims, photograph the damaged area before any temporary repairs, then document every repair step you take afterward.

Here is a practical checklist to guide your evidence collection:

- Photos and video of all damage, taken before anything is moved or repaired

- Written or recorded statements from witnesses, including their full name and phone number

- Police or incident report number and a copy of the full report once it is available

- Medical evaluation records, even if injuries seem minor at first

- Repair estimates from at least two licensed contractors or auto body shops

- Receipts for any emergency expenses you paid out of pocket

Deadlines that can close your claim permanently

California law sets firm limits on how long you have to take legal action if AAA insurance claims are denied or underpaid. For personal injury claims, the statute of limitations is two years from the date of injury under California Code of Civil Procedure Section 335.1. Property damage claims carry a three-year window. Missing those dates means losing your right to sue entirely, regardless of how strong your case is.

Missing a deadline is one of the few mistakes in a claim that cannot be fixed after the fact, so mark these dates on your calendar the day you file.

Your policy’s internal deadlines are separate from California’s statutes and can be even shorter. Check your declarations page for language about “proof of loss” submission windows, which often require written documentation within 60 to 90 days of the incident. Submit everything in writing and keep copies with timestamps so you have a clear record that you met every deadline.

Step 3. Track your AAA claim and stay organized

Once you receive your claim number, your job shifts from reporting to actively monitoring. AAA insurance claims move faster when you follow up consistently and document every communication in writing rather than relying on the adjuster to keep you updated. Adjusters carry large caseloads, and policyholders who check in regularly and keep their own records tend to get quicker responses, fewer delays, and a cleaner paper trail if the claim later becomes disputed.

How to check your claim status

AAA gives you two direct ways to monitor progress on an open file. Log into your regional AAA online account and navigate to the claims dashboard, where you can view status updates, check for outstanding action items, and review any documents that have been uploaded to your file. You can also call your assigned adjuster directly using the contact information you collected when you first reported the incident.

If your adjuster is unresponsive for more than two business days, escalate to their supervisor and document that request in writing.

When you call or email your adjuster, keep the conversation focused on three specific points: the current status of your file, any documentation they still need from you, and a concrete timeline for the next step in the process. After each call, send a short follow-up email summarizing what was discussed and any commitments the adjuster made. That email creates a written record that protects you if the details of that conversation are ever called into question later.

Build a personal claim file

Staying organized outside of AAA’s portal is just as important as monitoring it. Create a dedicated digital folder on your phone or computer the same day you file your claim, and add every document, photo, receipt, and piece of correspondence to it immediately rather than letting items accumulate in your inbox or camera roll. Disorganized records are a common reason policyholders lose negotiating leverage when a settlement offer comes in lower than expected.

Use the log template below to record every interaction with AAA from the date you file through final resolution:

| Date | Contact Method | AAA Rep Name | Summary of Discussion | Action Items |

|---|---|---|---|---|

| MM/DD/YYYY | Phone / Email / Portal | Full name | Brief factual summary | Next steps and deadlines |

Filling in this table after each call, email, or portal update takes under two minutes but gives you a complete timeline of the entire claim if you ever need to escalate or involve an attorney. Keep the log in the same folder as your photos, reports, and receipts so your entire file stays in one place.

Step 4. Handle repairs, rentals, and payments

Once your adjuster completes the initial review, AAA will authorize the next steps: repairs, a replacement vehicle, or a direct payment to you. This stage moves faster when you understand how each piece works and what to ask for upfront. How you handle this phase of AAA insurance claims directly affects whether you recover full value or leave money on the table.

Getting your vehicle or property repaired

AAA works with a network of preferred repair facilities called DirectRepair shops, and they will often suggest one when you report a claim. You are not required to use a preferred shop. California law gives you the right to choose your own licensed repair facility, and your adjuster must honor that choice. Going outside AAA’s network takes slightly longer, but you maintain full control over who works on your vehicle or property.

Choosing your own repair shop is a right in California, not a favor AAA grants you, so do not let any adjuster suggest otherwise.

Ask the repair shop to provide a written estimate before work begins, and compare that estimate against AAA’s repair authorization. If the adjuster’s approved amount falls short of the shop’s total, your shop can negotiate directly with AAA through a process called a supplement. Track that supplement request in your claim log so you know exactly when it is resolved and what the final approved amount covers.

Rental cars and temporary housing

Your policy only covers a rental car or temporary housing if you specifically purchased that endorsement. Check your declarations page for rental reimbursement language before assuming you are covered. If the endorsement is active, ask your adjuster to activate the rental benefit the same day repairs are authorized. Rental reimbursement typically covers a daily rate up to a policy cap, such as $30 per day up to $900 total, so confirm your specific limits before you pick up a vehicle to avoid unexpected out-of-pocket costs.

How AAA sends your payment

AAA sends payments in two common formats: directly to the repair facility after work is complete, or as a check issued to you and any listed lien holder on your policy. If your vehicle carries an active loan, your lender’s name appears on that check, and you need to coordinate with them before you can deposit it. For property damage claims, AAA may issue a partial payment upfront and a second payment once the final repair costs are confirmed and documented.

Step 5. Negotiate, appeal, or dispute a denial

Receiving a low settlement offer or a flat denial does not end your AAA insurance claims process. You have the right to negotiate, file a formal appeal, and escalate to California regulators if necessary. Most policyholders accept the first number they are given because they do not know they can push back, and that assumption costs them real money.

When AAA’s offer comes in low

Your adjuster’s first offer is a starting point, not a final answer. Review the settlement letter line by line and compare each item against your documented repair estimates, medical bills, and receipts. If the numbers do not match your actual losses, write a formal counteroffer letter that references each discrepancy with specific dollar amounts and supporting evidence attached.

A written counteroffer with attached documentation is significantly harder for an adjuster to dismiss than a verbal complaint over the phone.

Your counteroffer letter should follow this structure:

- Opening line: State your claim number, the date of the original offer, and that you are formally countering.

- Itemized breakdown: List each disputed line item, AAA’s figure, your documented figure, and the supporting evidence for your number.

- Total requested: State the exact dollar amount you are requesting and a reasonable deadline for response, typically 10 to 14 business days.

- Closing: Note that you reserve all rights under your policy and California law.

How to file a formal appeal

If AAA denies your claim outright or refuses to move after your counteroffer, request the denial in writing if you have not already received it. The denial letter must explain the specific policy language or factual basis for the decision. Once you have that letter, you can file a formal internal appeal through AAA’s claims department by submitting a written request that addresses each stated reason for denial with contradicting evidence.

Attach every document that supports your position, including photos, contractor estimates, medical records, and your claim log. Keep a copy of the full submission with a timestamp.

Escalating to the California Department of Insurance

If AAA’s internal appeal fails, you can file a complaint with the California Department of Insurance (CDI) at insurance.ca.gov. The CDI reviews complaints for unfair claims settlement practices and can compel insurers to respond. Filing a CDI complaint costs nothing, and the formal inquiry often prompts AAA to revisit a disputed file more seriously than an internal appeal alone.

When you want a lawyer in your corner

Most AAA insurance claims resolve without legal help, but some situations clearly call for an attorney. If AAA denies your claim after a formal appeal, offers a settlement that does not cover your medical bills and lost wages, or delays your file past a reasonable timeline, you are facing a fight that goes beyond what a policyholder should handle alone. An experienced personal injury attorney levels the playing field by communicating directly with AAA on your behalf, building a documented case for full compensation, and taking the insurer to court if necessary.

Steven M. Sweat, Personal Injury Lawyers, APC has spent over 25 years representing injured Californians against insurance companies that undervalue or deny legitimate claims. You pay nothing unless we recover money for you, and your first consultation is completely free. If your claim has stalled or the offer feels wrong, contact our team today and find out exactly where you stand.